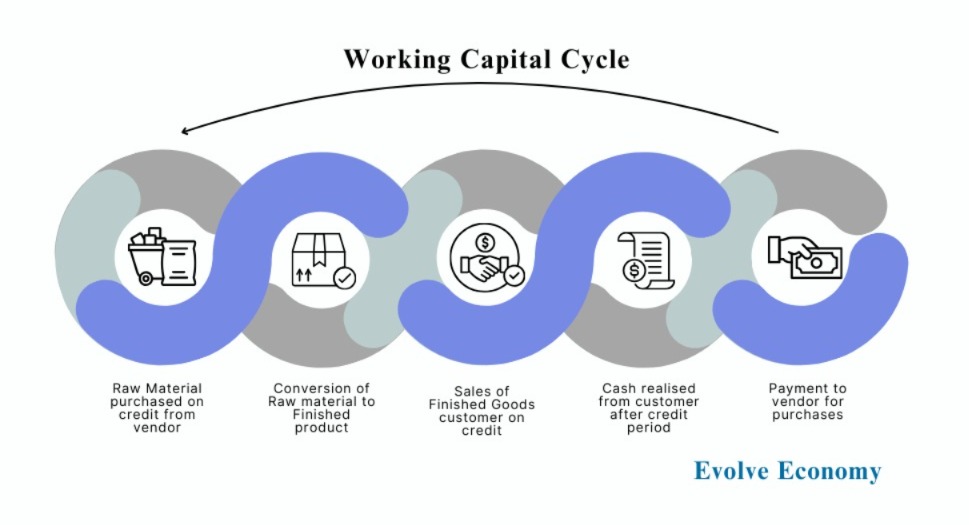

Working Capital

The Profit-Cash Bridge

Many entrepreneurs focus entirely on driving sales and delivering exceptional services, ensuring customer satisfaction at all costs. Yet, despite impressive revenue figures in their financial statements, their bank accounts often remain dry. This happens due to one of the most overlooked aspects of business finance: Working Capital.

Simply put, Working Capital is the money tied up in the daily operations of a business. It represents the funds invested in inventory, accounts receivable, and other short-term assets needed to keep the business running smoothly.

The Cash Flow vs. Profitability Dilemma

Entrepreneurs often confuse profitability with cash flow. While both are crucial for a business, it is important to understand the difference between them.

- A business records revenue as soon as a sale is made.

- The actual cash from the customer is received only at the end of the credit period This creates a time lag between recorded revenue and actual cash inflow.

As a result, while the financial statements reflect higher sales and profitability, the available cash remains constrained—causing liquidity issues despite strong revenue growth.

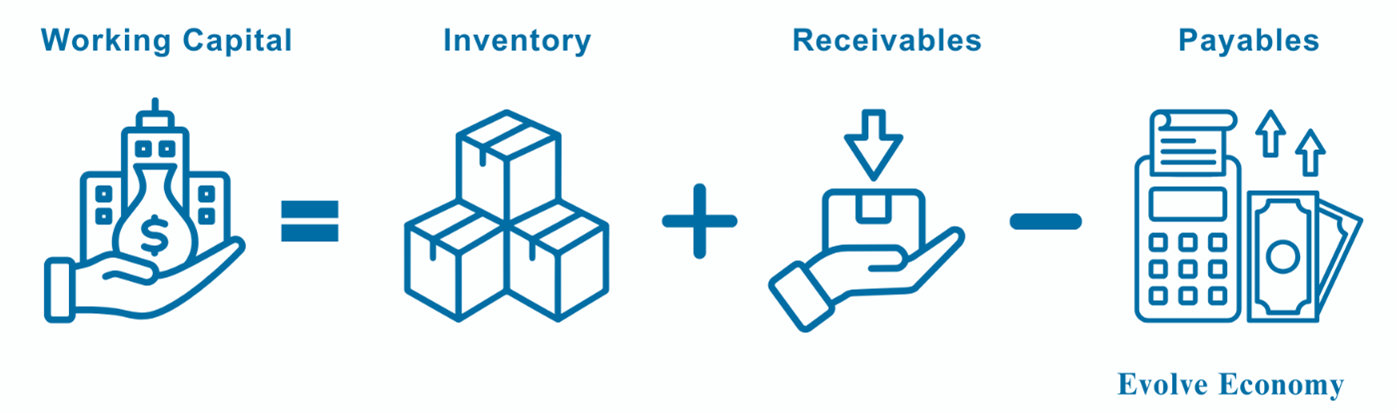

Components of Working Capital

Working capital is the lifeblood of any organisation, representing the short-term assets available to meet short-term liabilities. As a key indicator of a company's liquidity, efficiency, and overall financial stability, managing working capital effectively is essential for ensuring long-term success and sustainability.

Working Capital = Inventory + Receivables – Payables

For managing the working capital of a business, it is important to understand its key components.

1. Inventory

1. Inventory

-

- Inventory can be for raw materials, work in progress, finished goods and traded goods.

- Inventory gets converted into receivables once sales are booked against the inventory.

- The longer the time it takes to convert raw materials into finished goods, the higher the amount of working capital will be required.

- Minimum stock of inventory needs to be maintained to prevent stock out.

- It represents credit given to customers and other advances to suppliers.

- Receivables convert into cash only at the end of the credit period extended to them.

- While a longer credit period can help in strengthening ties with customers, a business loses interest in the money, which remains tied up in unrealised debtors.

- It represents credit taken from vendors and other advances received from customers, if any.

- Credit taken decreases working capital as it delays the cash outflow for services taken in the current.

- The higher the number of days of credit available, the lower the working capital requirement will be.

Why is it Important to Control Working Capital?

In the dynamic business landscape of India, managing working capital effectively is not just a financial imperative but a strategic priority. The businesses that can maintain their working capital at optimum levels get strategic leverage by becoming leaner in terms of fund requirements. For CFOs, particularly in startups and small and mid-size businesses, working capital optimisation can unlock growth opportunities, enhance profitability, and build resilience in the face of economic uncertainties.

1. Unlocking ROI

Keeping working capital at optimum levels helps in improving return on investments as it frees up excess funds, which can be utilised for other profitable activities.

2. Cost Optimisation

Reduced inventory levels help in saving carrying costs associated with it.

3. Improves Liquidity

A business with a lean working capital structure can manage its cash flows more effectively, ensuring the availability of funds for other regular activities like payment of salaries and overheads.

4. Enhanced internal accruals

The need for additional funds goes down when working capital is optimised, thus enhancing internal accruals.

5. Stronger Balance Sheet

An optimised working capital structure strengthens the balance sheet, which, in turn, boosts business valuations and helps in taking loans.

Keeping working capital at optimum levels helps in improving return on investments as it frees up excess funds, which can be utilised for other profitable activities.

2. Cost Optimisation

Reduced inventory levels help in saving carrying costs associated with it.

3. Improves Liquidity

A business with a lean working capital structure can manage its cash flows more effectively, ensuring the availability of funds for other regular activities like payment of salaries and overheads.

4. Enhanced internal accruals

The need for additional funds goes down when working capital is optimised, thus enhancing internal accruals.

5. Stronger Balance Sheet

An optimised working capital structure strengthens the balance sheet, which, in turn, boosts business valuations and helps in taking loans.

How to Optimise Working Capital?

Optimising working capital is not a one-time exercise but an ongoing process that requires a proactive approach. By improving receivables, payables and inventory management, a business can unlock its growth potential. A well-optimized working capital strategy ensures that the company is not just surviving but thriving in a competitive marketplace. A startup can implement the following to optimise working capital:

1. Inventory Management

- Implementing robust monitoring controls around Days of Inventory Outstanding (DIO) and Inventory Turnover Rate at individual SKU level

- Implementing a Just-in-Time management system to reduce inventory lead days

- Strengthening ties with suppliers for a faster raw material delivery mechanism

- Conducting regular Inventory Audits to identify shortfalls in actual stock with books

- Identifying non-moving and slow-moving SKUs to ensure their early liquidation Focussing on high-margin products and eliminating low-margin products

2. Streamlining Receivables

- Frequent reviewing of credit policies and keeping the credit days at a minimum

- Extending higher credit to only strategic customers

- Taking payments in advance from the customers, if possible

- Evaluating credit worthiness of customers before extending credit to them

- Implementing a systematic approach for debtor collection and regular follow-ups on overdue accounts

3. Optimising Payables

- Negotiating favourable payment terms & discounts for early payment with suppliers .

- Looking for alternate suppliers offering higher credit period

4. Robust Tracking and Analysis

- Analysing competitors’ model for identifying best industry practices

- Building strategic insights by tracking inventory, debtors and payable turnover ratios for early signs of working capital build-up

- Enhancing demand forecasting mechanism for optimal prediction of inventory needs

- Monitoring current cash runways available and eliminating unnecessary expenditures on working capital

- Detailed tracking of end-to-end cash flows to identify gaps in the system

5. Leveraging Financing Options

- Availing inventory financing against existing inventory as collateral

- Factoring/bill discounting receivables for early collection

- Taking short-term working capital loans from banks and financial institution.

6. Automation

- Developing automated dashboards for vendor payment and collection

- Adopting Technologies like RFID and barcode systems to enhance visibility and accuracy in inventory management